Closing the climate gap

“We need to act now” — You’ve been hearing it for years but what used to be a niche crusade led by scientists is now a global movement with Greta Thunberg at its head.

However, despite the pleas for urgency, little of the discussion has materialised into action, and we are yet to see tangible results.

This is because there’s a gap between what people and businesses say they want to do and what they are actually doing. That’s what I call the climate gap.

The Covid-19 pandemic may be a “Black Swan”, but it has shed much-needed light on this issue. Although it’s estimated the lockdowns will have reduced emissions from 4 to 7% by the end of the year, we theoretically need to reduce them by 7.5% every year between now and 2030 to keep temperatures from rising by 2 degrees and avoid the worst impacts of climate change. In other words, we’d have to stay in lockdown to save the planet. This concretely highlights the scale and urgency of the climate crisis.

However, instead of focusing on creating and implementing solutions, we seem to have spent most of our time explaining why climate targets and policies are a necessity to avoid a point of no return. It is great to raise awareness, but I would suggest it’s now time to discuss why we are not moving faster and how we can close the gap.

In my opinion, one of the things slowing us down is the lack of tools that can help us measure, monitor and reduce our impact. With the right tools, we could move past words, take action and steer the emissions curve to a more promising future.

I do have some good news. Entrepreneurs from all backgrounds have taken it upon themselves to close the gap. This article looks at some of the new early-stage tech startups flooding the space and the tools they are building to support individuals and businesses with measuring, monitoring and ultimately reducing their impact.

The rise of B2B

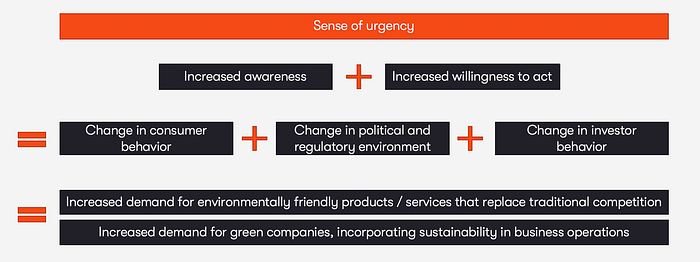

Solutions in this space either enable group action (B2B) or individual action (B2C). As you’ll see later, the market map I’ve created is crowded, even though it isn’t exhaustive. So, in order to really dig into the topic, I’ve decided to focus on group action, as I think it has a higher likelihood to drive the climate transition over the next 10 years. Here’s why.

- Individual action is limited due to the lack of concrete incentives.

While I believe that over the past few years, many consumers have developed an increased sense of climate consciousness and are slowly changing their behaviour, I still don’t think the majority will voluntarily take the necessary steps to significantly reduce their carbon footprint.

In my opinion, the average consumer is not ready to give up international plane travel, or willing to pay to offset their impact. However, they may be willing to adjust habits such as reducing meat consumption, exploring greener ways of commuting or making better consumption choices (if it’s a win-win: sustainable and affordable). This leads me to think that consumers are most impactful when holding businesses accountable through better consumption choices and value-based purchasing power. But they are not the only ones.

- Alongside consumer pressure, investor and regulatory pressures are pushing businesses to act more responsibly and lead the green transition.

Consumer pressure. A range of surveys have shown that consumers are increasingly interested in buying sustainable products, and some are even willing to pay more for it. Looking at the exact numbers is not the point here as there is always a mismatch between what people say and what they do (which is why we have a ‘climate gap’). All surveys demonstrate however that people are increasingly interested in more sustainable options. Many large brands are already adapting to this, with fashion houses developing new product lines using recycled materials, or food producers focusing on plant-based ingredients.

Investor pressure. Since the day academic papers started pointing to the positive relationship between good ESG performance and financial performance or resilience, the financial industry has been scrambling around to figure out how to measure it. The two main risks investors are worried about are external reputation risks and climate risk. Climate risk has been gaining more attention lately, it’s a business’ exposure to extreme weather events resulting from global warming, including the impact on assets in its supply chains.

Regulatory and socio-political pressure. At a European level, there’s regulatory pressures on transparency and reporting from the European Green Deal and the reviewed non-financial reporting directive. There has been some political initiatives around carbon emissions at a national level as well, such as the NetZero goal in the UK. Some more concrete regulations are currently under way in Europe which aim to put carbon emissions at the heart of business decisions by imposing a carbon tax or carbon quotas. Besides emissions, some key regulations that are moving things forward in sustainability include for instance the ban of single use plastics or Europe’s dedication to recycle 65% of municipal waste by 2035.

The combination of all three is leading to an increased demand for companies to offer more environmentally friendly options and to incorporate sustainability in business operations.

- A fast-growing group of climate leaders have already committed to action.

74 cross-industry companies signed ‘Uniting Business and Governments to Recover Better’ linked to the 1.5 degrees campaign, from consumer goods (Danone, Co-op, Unilever, Inditex, Ikea) and energy (EDF) companies to telecom (Sky) and tech (Salesforce). This shows that despite the crisis putting a strain on resources, many remain committed to prioritising a green recovery.

These climate leaders have made their motivations and commitments public, and some have even committed to results. It’s now important for them to execute and deliver on these goals.

The question is — where to start? Here, I’ve explored the different tools that currently exist for businesses of all sizes to measure, monitor, reduce, offset and report their impact.

The importance of Scope 3

Impact can be split into three scopes. Although the framework below is usually used for carbon emissions under the Greenhouse Gas Protocol Standard, I find it useful to talk about all sorts of impacts such as waste creation, energy usage, water contamination etc.

· Scope 1 — direct impact originating from sources the company owns or controls

· Scope 2 — indirect impact through company’s energy consumption (electricity, heat)

· Scope 3 — indirect impact of upstream or downstream activities of entire value chain

Businesses are seeing pressure to reduce their impact across all areas, but especially around Scope 3.

- Consumers are particularly focused on Scope 3 in terms of the downstream / end-of-life impact as well as upstream / supply chain in relation to labour rights.

- Investors and insurers have a focus on Scope 3 as they need to estimate how vulnerable the upstream / supply chain is to climate risk (ie. extreme weather events).

- Regulators have so far focused on Scope 3 in terms of downstream / end-of-life with regulations on waste and single use plastics. More recently we’ve seen an increased focus on upstream / supply chain in terms of carbon emissions with European lawmakers agreeing to include shipping in the EU emissions trading system (ETS), which obliges factories, power plants and airlines to pay for their pollution.

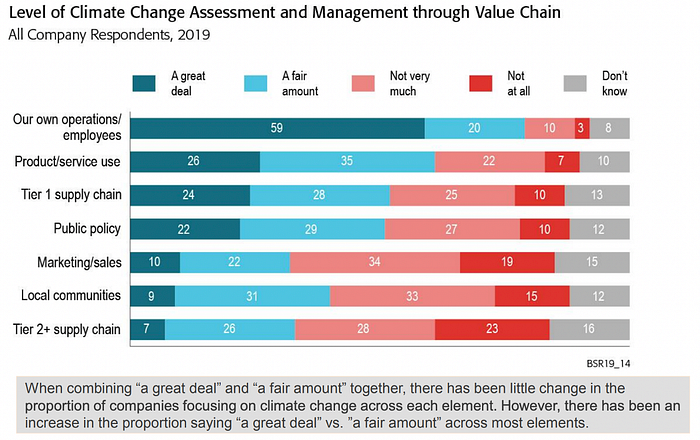

Stakeholders are correct to point the finger at Scope 3. 80% of emissions and 90% of climate risk are in supply chains, which is why measuring the impact hidden there is of critical importance. However, the complexity and lack of data has meant it has often been ignored.

Indeed, today’s global economy has developed interdependent, complex and opaque supply chains. Businesses increasingly source their materials and components from across the globe and are reliant on just-in-time production. As we’ve seen with Covid-19 and previous extreme weather events, supply chains are vulnerable to disruptions. Research has shown that 60% of S&P 500 companies hold assets at high risk of physical climate change impacts, which is why having the tools to identify these exposures and build continuity plans is critical. In addition to that, the lack of information exchange and transparency from all the different actors in the supply chain is making it near impossible for large organisations with thousands of suppliers to measure their impact.

Tools to close the gap

Solutions can be split into three feature categories:

1) Understand & Measure. From tools that collect data to measure impact, to tools that help understand and contextualise that data.

2) Reduce & Report. From tools that help visualise and report the impact, to tools that guide what actions are needed to reduce it.

3) Offset & Invest. From offsetting marketplaces to tools financing green projects.

Across the board, users expect cost competitiveness, user-friendliness and integrability. The most important differentiators so far are data quality, methodology accuracy, trustworthiness and scalability (managed services vs SaaS).

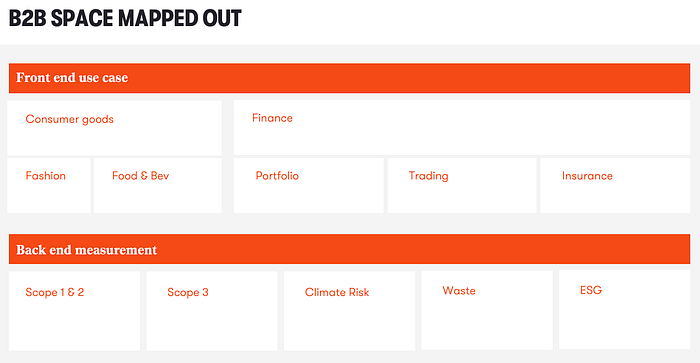

Within the B2B space, tools can usually be split between front-end (SaaS with UI for a specific use case) and back-end (data collection and impact measurement toolkit).

Some startups are building a horizontal solution, focusing either on the front-end or back-end measurement across multiple use cases, whilst others have taken a vertical approach doing everything from data collection to user interface for their particular use case.

Even though I spoke to 40+ start-ups in this space, it’s still very early so it is unclear how everything is going to play out. I’m most excited about the start-ups that focus on automating data collection and providing accurate measurement on the back-end side as I believe they can become leaders as data providers. Their approach can be defensible from the start (models based on science, proprietary data collected) and they have an opportunity to move towards the front-end later on although they would have to have the execution skillset to effectively build a platform with product-market fit across a set of use cases and industries. On the other hand, I also believe some front-end start-ups serving a specific use case within a vertical like those focused on sharing impact data with consumers in the fashion or food industry, have the opportunity to grow big, but differentiation will mostly be built over time with increasing trustworthiness and ease of use.

Overcoming the headwinds

The existing solutions, consultants and ESG ratings, are expensive, inconsistent and opaque. Start-ups in the space are using technology to use a more data-driven approach and automate the process as much as possible in order to bring the cost down. This is not without its challenges:

· Lack of data or poor data quality

Part of the data collection is still manual. Despite companies increasingly reporting on sustainability, not all publicly disclose the level of detail needed for impact calculations. Sometimes the data isn’t recorded at all in which case tools need to estimate the impact as accurately as possible using data modelling.

· Lack of transparency

You’ve probably heard of the term ‘Greenwashing’ or heard about offsetting scams. For instance, only 30% of the amount being paid for carbon offset ends up being spent on the project itself, the rest goes to intermediaries. Similarly, 5% of offset projects used by the EU failed to reduce emissions due to wide ranging factors including double counting, additionality, permanence, leakage. The mediatisation of these issues has led to a lack of trust and increased scrutiny on the companies, adding pressure on businesses that want to do the right thing and avoid backlashes.

· Lack of standards

There’s been an attempt to align across standards. Indeed, in 2018, the three leading standards (GRI, CDP, SASB) came together to simplify and centralise reporting recommendations in line with the Task force on Climate related Financial Disclosures’ (TCFD) guidance around climate risk. In addition, the industry is moving away from relying on one ESG rating per company to using a range of metrics and ratings to measure performance across different impact types. As the lack of a unique standard remains, solutions need to offer the flexibility to conform to several standards that might change over time.

· Machine limitation

Measuring emissions can be automated to a certain extent by extracting the data necessary from receipts and using carbon estimations. But machines reach their limit when evaluating impact in a broader sense, when human judgement is necessary to evaluate one impact vs another, combining positive and negative impacts. This would be the case for instance when evaluating the overall ESG impact of a Fortune 500 company.

These challenges are tough, but they also represent long term defensibility opportunities. If it was easy, these tools would already exist. But when in the past it was finance experts entering the ESG ratings world, we are now seeing teams with both technical (climate science, and machine learning) and industry (supply chain, fashion etc) expertise tackle this gap so I feel confident that new, better tools are being created.

Change is finally coming

As discussed in my last Medium post, Covid-19 has put the world on pause (especially supply chains). We’ve learnt the importance of listening to experts, acting early to avoid larger negative impacts later as well as the importance of overall risk mitigation and resilient value chains. As a result, people from all walks of life are seeing an opportunity to re-start for the better. Many are hoping for a Green Swan or a Renaissance just like after the Black Plague, or more generally people are hoping for a Green Recovery.

As discussed, we have reasons to be hopeful. Great teams are flooding the space to give us the tools to tackle and drive the post-Covid green transition. Funding is a critical next step here, and although it’s a debatable topic by itself, it’s worth mentioning that we have already seen large amounts of funding being directed towards the climate issue, even in the midst of Covid-19. Indeed, in the first half of 2020, net inflows into ESG funds hit $21bn, almost matching last year’s total. At Balderton, we’ve been looking at the sustainability space more broadly to see how we can get involved to support entrepreneurs who, like us, want to close the ‘climate gap’. If this sounds like you, give us a shout!